Here are some things I think I am thinking about this weekend. I am embarrassed to admit that I had never watched the legendary series Mad Men. That’s a problem I am in the process of fixing and I was struck by a hilarious scene where Pete Campbell runs into the elevator being held by his office nemesis, who asks him “How are you Pete?” To which he responds, “NOT GREAT, BOB!” It’s a hilariously uncommon response to a common question. And so, in the name of brutal honesty and the handful of Mad Men who are disrupting the global economy, let’s talk about whether the things going on these days are not great, Bob.

1) The data is not great, Bob!

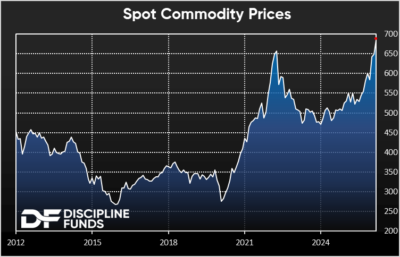

Earlier this year I discussed the big surge in commodity prices and how it could throw a wrench in any plans to cut interest rates if it persists. Well, it has gotten significantly worse with the Iran war. Commodity prices are now up 30% year over year and gasoline prices alone are up 55% year to date. These are huge figures that will put upward pressure on headline CPI and PCE. But it gets worse. On Friday morning we got another big negative job print with large downside revisions for the months prior. The labor market is frozen.

The problem here is you’ve got the worst possible confluence of events for this particular environment. The labor market is weak and in an unprecedented period of uncertainty due to slowing growth and AI labor market uncertainty. And now we’re all going to get jammed with high cost inputs and gas prices. This is going to redistribute consumption further away from things like entertainment and services. This will make the headline inflation readings look really bad and could put downward pressure on core inflation readings.

I am by no means a war strategist, but I find it very hard to see how the administration can weather this storm. There is going to be a narrative storm about stagflation and rising gasoline prices with falling labor in the coming months. The financial markets are screaming “we cannot afford to be engaging in another war in the Middle East right now“. I guess we’ll have to see if anyone is listening.

2) What about interest rates, Bob?

What does it all mean for the future of interest rates? Mortgage rates are at 6.2% as I type. They’ve jumped from 5.95% just last week. So the bond market is starting to price in a little more inflation risk, but the labor report makes that very uncertain. Fed Funds Futures have priced in just one cut for 2026. Prior to the Iran invasion I was in the “Fed should cut” camp, but now the world is much more uncertain. But you’ve got the worst of all worlds for the Fed. The inflation story just got a lot more confusing and the labor market is really softening.

I would err on the more cautious side here. Our leading inflation gauge has jumped up to 3.67% in the last few months, but the labor market softness probably offsets that in terms of what the Fed should be doing. They can’t be increasing rates into a deteriorating labor market where a lot of the last month of commodity price increases is clearly more supply driven than anything else. You don’t want to say the commodity price changes are “transitory”, but with the prices being driven by the war you have to defer towards labor markets as the demand driver. And if this all gets worse and oil prices surge even further then we have to assume that demand for everything else in the economy is going to devolve. That’s a recipe for recession.

In short, I would assume there’s near-term upside risk in interest rates, but in the long-term none of this looks like a permanent tailwind to higher interest rates.

3) Is AI risk “not great, Bob”?

The most recent scary viral article came from Citrini Research on AI. It purportedly moved the market last week and caused a big sell off in tech. The piece paints a catastrophic view from the future where AI has ravaged the workforce and the financial markets. It was interesting timing because we also got news from Jack Dorsey, the CEO of Block, that they were cutting 40% of their workforce due to AI efficiencies. The news from Block was the first large and definitive job cutting we’ve seen that was directly attributed to AI. What do we make of it all?

First of all, there isn’t widespread evidence of sustained layoffs so far. As I’ve noted in the past, what we’re seeing so far is caution, not collapse. Firms are pulling back hiring, but they’re not firing en masse just yet. So the weak labor reports we’ve seen in the last 6 months reflect a degree of caution. I think big firms are trying to get more out of the workforce they currently have because they are getting a little more productivity out of each worker. At the same time, they’re not eager to hire because they don’t want to overleverage themselves in labor if AI should turn out to be the efficiency enhancer many predict it to be.

Personally, I’ve become more aligned with what I would call a “disruptive decentralization” outcome. AI is hugely disruptive and decentralizing for big firms. So, if you’re a law firm with 50 partners and 200 associates then your revenue stream relies heavily on the 200 associates who bill half as much as the partners. You need those associates to keep billing and AI creates no incentive for you to stop having those people bill even if they’re not as efficient. But what this also does is it allows a 5 partner law firm with 20 associates to now start operating as efficiently as that larger firm. And what does that do? It gives the smaller firm pricing power. So now the smaller firm can charge a lower fee that’s more attractive when compared to the larger firm and they can do the same work. This is overly simplified, but in short what AI does is it exposes bloat in big firms and gives small firms the ability to operate like bigger firms.

So my general view is that AI is a great thing for smaller and more nimble firms and individuals. And it’s going to expose a lot of larger legacy firms. I don’t know exactly how that will all play out in the short-run, but it isn’t negative in the aggregate as much as it’s negative for large firms when compared to small firms. How this plays out over time is the big unknown. In the long run the economy will digest it and we’ll live on. But there’s a scenario where firms cut many workers in the near-term and that risk probably gets exacerbated due to the uncertainty from everything above.

As usual, it’s long-term gain in exchange for short-term pain. The trick is staying disciplined in the short-term to benefit from the long-term. Easier said than done.

I hope you have a great weekend. And as always, stay disciplined out there.