Here are some things I think I am thinking about this weekend.

1) The Era of Irrational Apathy is Back?

About 10 years ago I wrote an article called “The Era of Irrational Apathy”. The basic gist of the article was that living standards were not nearly as bad as the media and politicians would have you believe. The data largely supported this. And it’s even more dramatic when you look at the USA on a global scale and you understand facts like, the median American is in the top 10% of all global wealth. The USA is an unfathomably wealthy country with living standards that far surpass the global average. Of course, there are problems. Plenty of them. But there’s a lot of amazing things about the USA and our broader living standards in general, that we don’t talk about enough.

I discuss this because World Cup fever is taking the USA by storm. And foreigners have flooded the USA to watch the games. And…they cannot believe how great the country is. Social media is mobbed with foreign accounts talking about the diversity of food, the incredible infrastructure of our stadiums, the size of EVERYTHING, the incredible entertainment in every city and the friendliness of Americans. Even The Economist is writing articles about it. And it all makes you wonder if we’ve been fooled by the media and politicians into thinking that everything is terrible, when, in reality, there is a lot to love about our own country? After all, the media is incentivized to tell us that everything is scary because then you need to tune in to stay on top of the bad news. Financial media has mastered this of course. Fear is a powerful motivator. But politicians have made a daily thing of it as well. And it’s not just one side. Both political parties spend their days telling us how something is terrible. You know all the narratives.

My theory on this is that it’s largely a social media driven inequality narrative with shreds of truth that are stretched wide. We see this most recently with the news that Elon Musk is a trillionaire. Now, most of that wealth is unrealized capital gains in stock value. This unrealized gain has virtually no impact on anyone else’s life. It could be fictional. It could be gone in a year if stock prices decline. The point is, when stock values rise they’re endogenous price changes that expand the size of the entire wealth pie. They aren’t changes that come from Erin’s pocket and into Elon’s pocket. Elon’s pockets just got bigger while Erin’s pockets stayed the same size (or, in the case of thousands of SpaceX employees, their pockets also got much fatter). But this is important because if you listen to politicians they’ll make it sound like Elon did something terrible here by being the largest beneficiary of these gains. They make it sound like he stole pie from the rest of us when in fact he made the whole pie bigger through innovation and stock market revaluation. That’s a good thing. Innovation and value creation is, arguably, the most important element of the economy as it creates the very resources and assets that make the entire credit system viable. Now, that doesn’t mean inequality isn’t a problem. But context matters.

Anyhow, as we’re nearing the 250th birthday of this great country I think it’s important not to get too bogged down in negative narratives. This young country has developed some of the most amazing living standards in a fairly short period of time. Don’t let scary media narratives convince you otherwise.

2) Bad Incentives, World Cup Edition.

I’ve really been enjoying the World Cup this year. But every time I watch soccer I am reminded about how bad the incentive structures are. Yesterday, the USA won 2-0 over Bosnia and Herzegovina. Europe tried to send two countries at us, but America has become so formidable at soccer that we defeated both of them in one game (I kid, of course). During the game the USA’s best player was given a red card for stomping another player’s ankle by accident. When he did this the other player fell to the ground and acted like his ankle had been chopped off. But by the time the red card was confirmed the other player had made a miraculous recovery and went on to play the rest of the game unharmed. The result is the USA lost their best player for 30 minutes and also loses him for the entire next game. Imagine an NHL player getting sent to the penalty box for 120 minutes because he stomped someone’s ankle (the NHL, by the way, has mastered incentives and I am convinced the Commissioner of the NHL could fix every problem in soccer in 10 minutes). Even worse, imagine the NHL allowing a player to flop on the ground every time he got hit. The penalty is so excessive that it rewards flopping disproportionately. You see this a lot in soccer and it’s a gigantic problem that they refuse to fix. And the issue is bad incentives.

Soccer is a game that averages just 3 points total between both teams. A red card, penalty kick and suspensions have huge asymmetric ramifications. If you can bait the ref into handing out red cards then there’s no incentive not to act like you’re dying every time you get bumped. After all, if that red card results in a man advantage, penalty kick or suspension then your acting suddenly becomes the most important thing going on during the game. A single penalty kick can impact 33% of total average goals so the incentive to get penalties is greater in soccer than it is in other sports. This is vastly different than something like the NBA, where flopping is also a problem, but a far smaller impact because two free throws are less impactful in a game with a total scoring average of 200 points. Of course, Americans watch this and just can’t stand it. We’re used to watching American Football, a game where, if a man is laying down hurt for 2 minutes you just assume he literally broke his spine. Americans are all over the internet complaining about this and Europeans essentially respond by saying “shut up, this is the way it’s always been”. Which is exactly the problem. As The Economist article states, the Americans are constantly evolving, innovating, critiquing and trying to improve. The Europeans seem stubbornly stuck in their old ways, even when Americans are critiquing a game we genuinely want to like.

Charlie Munger once said “show me the incentive and I will show you the outcome”. Europeans like to claim that soccer is the world’s most popular sport. But this isn’t really true in economic terms. American football and the NFL generate $24B a year in revenue. The big five European soccer leagues generate $20B. On a per capita and per game basis the NFL is vastly more popular than soccer. Like many Americans I want to embrace soccer more than I do. But when I watch a game I see lots of bad incentives dominating outcomes. And that’s bad economics.

3) Update on Real Money Market Funds.

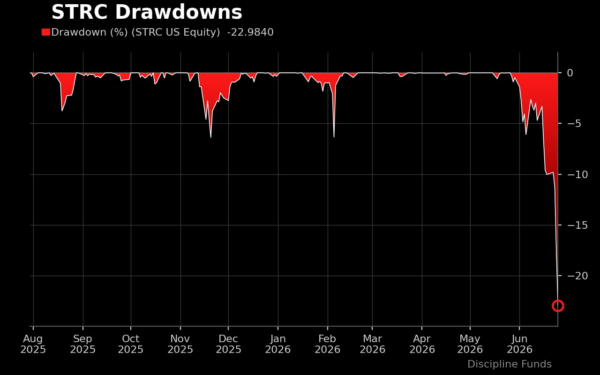

The internet was abuzz with discussions about STRC this week. STRC is the preferred stock from Michael Saylor’s Strategy. I wrote critically about this instrument back in April after Saylor had described it as being equivalent to a money market fund. Well, this week we found out that STRC is very much NOT a money market fund as it fell over 23%.

I approach everything in finance and economics from a first principles perspective. It’s really important to understand the ingredients of the financial system so we can understand what certain instruments are likely to do over time and how they fit into our financial meal plans. This is even more important if you’re implementing any form of asset-liability matching strategy because you cannot be matching long-term assets to short-term liabilities. That’s how you end up like Silicon Valley Bank or someone who feels motivated to sell stocks in a bear market. And money market funds should only be matched to short-term liabilities because they are inherently short-term assets.

STRC is a very different beast than a money market fund. It’s an inherently longer-horizon instrument because generating that kind of yield requires exposing capital to assets that need time to ride out volatility and break even. If Strategy was able to guarantee a dividend of 12% every year in perpetuity then it would require some form of perpetual 12% income stream to fund that. Can they reliably do that every single year in perpetuity? Of course not. No private sector firm can. That’s why money market funds are typically loaded with T-Bills and very short-term corporate paper at relatively low interest rates. Even the largest revenue generating entity in the world (the US government) cannot guarantee 12% per year in perpetuity.

Anyhow, be careful with your asset matching out there.

I hope everyone has a wonderful 4th of July. America turns 250 years old this weekend. And while we might debate about the “best” country in the world I think we can all agree that it’s been a pretty incredible country for the fairly brief 250 years it’s been around.

Have a great and safe weekend. And as always, stay disciplined out there.