Here are some thing I think I am thinking about this weekend.

1) Discipline Funds hits $100MM.

6 months after launch and I’m excited to announce that the Defined Duration ETF Suite has reached $100 million in AUM this week. We launched the Defined Duration ETFs to help planners connect time horizons with assets so it’s exciting to see the concept resonating.

Running a boutique ETF company is no joke. You’re basically jumping into the most competitive business in the world where the biggest and baddest companies operate. They have the brands, the scale, the customer loyalty and the distribution. And when you launch a new fund you have virtually none of that. And the worst part is that you need assets to make a fund company survive but it’s hard to get the assets when you don’t have a track record.

I started the Defined Duration concept because I feel as though the retail asset management and financial planning space is genuinely missing a retail friendly asset-liability matching process. Time is the main variable in anyone’s financial plan and with the exception of Target Date Funds, which I find pretty clunky, there aren’t many elegant solutions to solving the temporal problem in portfolios. Equity funds let their risks float with valuations and most bond funds let their interest rate risk float as their composition shifts. None of them are actually time weighted. And the kicker is that time weighted investing is too intuitive and planning friendly for this to not exist. Every day I talk to clients about how they now, suddenly understand their portfolio in a totally different manner than they used to. It’s really cool. We build financial plans that seamlessly match to the asset allocation. It’s all integrated and every asset plays a role in helping the client achieve tangible financial goals. And our products play an essential role in that process because they’re specifically designed to control the time horizons over which they achieve certain goals.

I feel like we’re at the beginning of a long journey so this is a nice milestone to get to. There’s a lot of work still to be done to get this rocket ship off the ground, but it’s nice to feel some liftoff starting.

2) SpaceX is a Crazy and Exciting Stock….

Speaking of rocket ships – let’s talk about the SpaceX IPO because it’s all anyone is talking about these days. Now, I don’t generally like to jump into individual stocks, but this individual stock might have a big impact on index funds so let’s dig into it.

First of all, this is just the most exciting stock ever in my opinion. Everything about it sounds like science fiction. And that’s why the valuation is ludicrous across the board. The S-1 disclosed a positive consolidated adjusted EBITDA of $6.58 billion for 2025 (driven heavily by Starlink’s $4.4 billion operating profit – mind you, the cute little internet company is not even remotely interesting in all of this in my opinion). At a $1.8 trillion valuation, this results in an adjusted Price-to-EBITDA multiple of 273.5x. The average S&P 500 firm sits around 10-20 for reference. But it’s also the most insanely far fetched company, but yet not so far fetched that it’s unimaginable. I jokingly wrote on Twitter that the math makes sense once you understand:

NPV = SUM[ t=1 to n ] ( R_t / (1 + i)^t ) – C_0 + THEY FIRE ROCKETS INTO SPACE AND THEN LAND THEM BACK ON EARTH FULLY INTACT.

I’m mostly kidding there. But kind of not. Musk’s insane idea is to build data centers (and lots of other stuff) in space and then wrap this all around an internal AI company that has the satellite’s integrated. But the kicker is the rockets because they can launch and land non-stop in theory. They become shuttles for materials and whatever else the company ends up wanting to build in space. If you buy SpaceX you’re buying a company that has a potential monopoly on space build outs, not just data centers, we’re talking everything. In 25 years they’re controlling defense mechanisms, fiber optics, in 50 years they’re building lunar bases, Mars bases, yes, very far fetched and insane sounding stuff, but not entirely out of reach either. You can imagine a world in which the whole thing is integrated and one day you have Tesla robots getting launched into space where they’re driving cars on the moon, powered by solar panels, operated via AI and building whatever we need back on Earth. The logic chain (and valuation) is seductive because it sounds far fetched, but achievable. Anyone following the Musk story over the years can now see it all beginning to come together.

The problem is that ground based AI compute is bottlenecked by power, cooling and regulations. Power is flat in the US, cooling is expensive, and permitting a gigawatt scale data center takes years. SpaceX claims to sidestep all three with near continuous solar energy, passive heat radiation into space, and no local grid or zoning to fight. And they’re the only company on earth that can launch the mass required to do it cheaply, because they own the rockets and the ability to keep launching them non-stop. That vertical integration (pun very much intended) is the moat. But it’s a moat that could take years to build and whether they can build it at all is a stretch.

If they make it work the company is UNDERVALUED massively because it becomes the most important technological advancement potentially ever since it can power everything and build out the economics in ways previously unimaginable. Can they make it work though? History with Musk says it will be massively more difficult and time consuming than he expects. But he’s also not a guy to bet against.

From an asset-liability matching Defined Duration perspective this stock has a SUPER long duration (potentially infinite given Musks own bankruptcy comments), even though it’s mature. Its range of outcomes is so wide that you have to treat it like a venture capital stock, even though it is mature. It’s an outlandish bet. A better bet than the lottery, but maybe not by much. My guess is Musk will win in the long-run. But it will take much, much longer than he expects and that means it will be a very bumpy road getting there. And despite being totally crazy in some ways it’s also incredibly exciting. What a time to be alive!

3) Will SpaceX Destroy Our Index Funds?

The biggest news of the week was that S&P will NOT fast track inclusion of these AI stocks. The worry here is that we’re about to get a bunch of super high valuation AI names jammed into our index funds which will distort the performance. And this could result in indices like VTI, VOO and QQQ looking very differently from one another. Especially since VTI and QQQ will inherit these names much faster than VOO will.

First, I have to laugh a bit about all of this because I spent much of the last decade having mundane debates with “passive” index fund advocates about how their index funds were much more active than they suspected. And now we’re seeing that these index funds have a huge amount of discretion within the process of allocating to certain names. So I think we can put that whole “passive” debate to bed now. Everyone is active and that’s fine. There are smart ways to be active and stupid ways to be active. So, let’s talk about whether adding the AI names will suddenly make our index funds stupid.

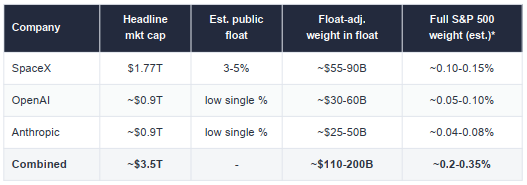

The S&P 500’s aggregate market cap is roughly $62 trillion. The total U.S. investable market that CRSP captures is larger still. The accompanying table sizes the weights on full inclusion, using float-adjusted estimates since both index families weight by free float, not total shares. The float adjustment matters enormously here: SpaceX and OpenAI are floating only a small sliver of stock, so their index weight will be a fraction of their headline market cap. That’s likely to change over time, but it’s not like the major indices are going to suddenly become 5-10% newly IPO’d AI on day one.

But what about the years ahead? I am guessing to a large degree but based on publicly available float schedules I think the following estimates of weighted inclusion of all three in 2028 is about this:

QQQ (Naz 100): 5%+. Potentially much higher if the others are fast tracked as well.

VTI (Total US): 1.5-3%.

VOO (S&P 500): Perhaps 0%, but if all three are public and profitable (unlikely) then the contribution could be in the 1.5-3% range by 2028 though a lot of that hinges on SPCX stock price changes.

The bottom line for me is, it depends on what you own, but if you own VOO or VTI then this isn’t going to move the needle a huge amount. Even with the fast track inclusion the float adoption is still going to take time since it can’t happen all at once. If you own QQQ then the risks are materially different and your sequence risk is potentially much higher.

From a Defined Duration perspective it all matters because all of these tech names need to be thought of as very long duration names that add significant sequence of return risk to your portfolio. If you’re owning this stuff you need to compartmentalize it and be ready for lots of days like Friday where these things get clobbered. It’s not just SpaceX that matters there. You already have significant sequence risk in the existing AI names and the big tech companies that make up 35%+ of the indices. If you’re trying to match this sort of asset to short-term funding needs then you’re really setting yourself up for big risks.

Well, that’s all I’ve got for you this weekend. I hope you make it a great one. And as always, stay disciplined out there.