We return to our regularly scheduled analysis now that Spring Break is over and I am no longer being run over by my daughters every day. And it’s good timing because we appear to have a deal in Iran. Let’s dig into it.

1) We Have a Deal with Iran…MAYBE?

I’ve said this over and over again in recent weeks, but there was never a high probability this thing could last that long. The narrative was just too damaging. With mortgage rates at 6.5% and gasoline over $4 you couldn’t sustain a situation where the US continued to allow oil prices to remain this high. Especially not in a mid-term election year. The question now is, did this last long enough to make a meaningful difference on the economy?

The good news here is that it doesn’t look like there has been meaningful damage in the labor market. We track the real-time FICA data pretty closely and it’s actually improved a bit in the last few weeks. This was validated by the most recent BLS labor report. Further, the US economy is far less sensitive to oil and gas prices than it used to be so it would have taken a much larger oil surge to cause a recession. So, we likely dodged a real recession, but we’re still going to see a hit to consumption in other goods and the news on inflation and interest rates is even less encouraging.

Oil prices are cratering to $95 as I type. This could be one of the largest one day declines in history. The problem is, oil was $60 just a few months ago so we’re cratering, but cratering after a 100% increase in prices. So you’d need a 30%+ decline from here to revert back to the inflationary trend we already had in place. Gasoline is even stickier and is down just 10% as I type. That equates to the $3.85 range. Is gasoline going to fall back $2.90 where it was a few weeks ago? Because anything higher than that is additive to year over year inflation. Gas prices tend to be much stickier to the upside, but at a minimum you should expect sticky looking inflation readings in the coming months that will keep the Fed very much on hold. Also, it’s going to take time to get the oil flowing again and that assumes we get things back to pre-war levels soon, which is still up in the air.

The problem is we already had a sticky inflation problem before any of this began. That means we are likely to see high-ish inflation readings all through the Summer and that means short-term interest rates aren’t coming down any time soon. So, with high mortgage rates and high gasoline prices you’re going to have a lot of angry consumers through the Summer who can’t understand why they’re paying higher prices for what looks like another needless war in the Middle East.

I said this a few weeks ago, but this whole thing reminds me of the tariffs. The White House appears to be using the same playbook here where they make a very severe threat and then follow it up with a series of 2 week “deals” that delay that armageddon scenario out into the future. The difference here is that the tariffs ended up being small and difficult to analyze from an inflationary perspective because there wasn’t an obvious impact. This one won’t be so difficult to critique as every consumer in the world can see the direct and lasting impact of surging oil and gas problems. I took two Ubers and a flight today. Both drivers AND the pilot made jokes about fuel prices. It’s all anyone is talking about.

In the end it all looks like another geopolitical threat that likely ends up being something we’ve all forgotten a year from now. But there’s going to be a lot more head scratching about this one as it looks like there are obvious net negatives with not so obvious net benefits.

2) Another Lesson in Geopolitical Investing?

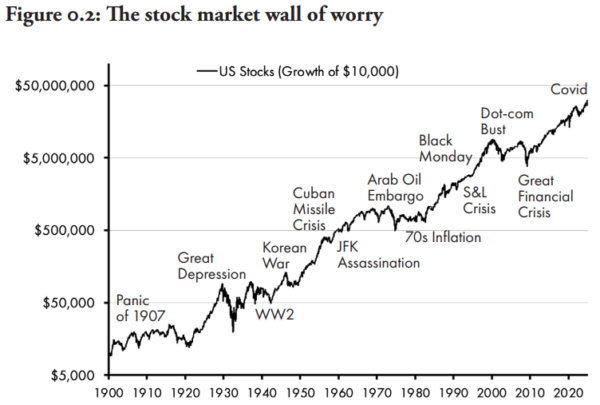

I spend way too much time here discussing geopolitical events that seem to never end up mattering in the long-run. And yes, it’s a story as old as investing. One of my favorite charts in my new book was this chart of scary global events that have resulted in little to no long-term impact. Or rather, I should say, they had a meaningful short-term impact, but if you had the ability to look beyond them they had little impact on your long-term returns.

Naturally, this is my favorite thing about the Defined Duration strategy. In this approach assets are specifically aligned to time horizons that correspond to your financial needs. The stock market is best thought of as a 15+ year instrument that will earn 6-7% per year on average. But if you’re constantly getting worked up over 15 minute or 15 month moves in the stock market then it probably means you have an asset-liability mismatch in your portfolio.

This is one of the main benefits of asset-liability matching portfolios or what some institutional investors call Liability Driven Investing. When you match your short-term spending needs to short-term assets you don’t need to worry about what your long-term assets are doing. But there’s a component of real portfolio alpha in here as well. When you fund your portfolio exclusively and strategically from short-term instruments you are explicitly allowing the long-term assets to stay fully invested. This means they’re being allowed to generate the higher expected returns that we rely on them for. So there’s a double benefit in the ALM approaches – not only do you have a behavioral edge because you can see the actual liquidity in your portfolio, but you’re explicitly allowing the risky part of your portfolio to remain risky and oftentimes even pushing it riskier because you created so much near-term certainty in the portfolio that you actually feel comfortable taking more risk than you otherwise would.

3) Last Minute Tax Day Alerts

Here are a few housekeeping notes in case you’re doing last minute 2025/26 tax planning:

– Max Out Your Prior Year IRA Contributions

The most common last-minute move is the prior-year contribution to a Traditional or Roth IRA. You have until the April filing deadline to contribute for the previous tax year.

- The Limits: For the 2025 tax year, the limit is $7,000 (or $8,000 if you are age 50 or older).

- The Benefit: Traditional IRA contributions may be tax-deductible (depending on your income and workplace plan), while Roth contributions allow for tax-free growth and withdrawals in the future.

- Pro Tip: When making the transfer via your brokerage, ensure you explicitly select the 2025 tax year. Most portals default to the current calendar year by April. Might as well make that 2026 contribution while you’re at it (it’s $8,000 and $8,600 if 50+). .

– Fund Your Health Savings Account (HSA)

If you are enrolled in a High Deductible Health Plan (HDHP), the HSA is often called the triple tax-advantaged account. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

Like the IRA, you have until Tax Day to reach your 2025 contribution cap:

- Self-only: $4,300

- Family: $8,550

- Catch-up: If you are 55 or older, you can add an additional $1,000.

– Self-Employed? Check Your SEP IRA Deadlines

For the self-employed, entrepreneurs, and small business owners, the rules offer a bit more breathing room. If you utilize a SEP IRA, you can contribute for the prior year up until your tax filing deadline including extensions.

If you file for an extension, you could potentially have until October 15, 2026, to fund your 2025 SEP IRA. This is a powerful tool for managing cash flow while still reducing your 2025 tax liability.

Well, that’s all I’ve got for now. I hope this has been a helpful note. And as always, stay disciplined out there!