1) Dalio Doom.

This week’s scary viral article comes from none other than Ray Dalio on X. I won’t regurgitate the entire piece, but it’s basically an argument about how the world order is changing and geopolitics will drive portfolio construction in the future. His short conclusion is buy gold and sell debt. I’ll cut to the chase – I think this is the kind of macro narrative that gives macro investing a bad name.

In my view there are two types of macro investing processes:

A) Those who use macroeconomics to make short-term active investment decisions based on broad narratives. Think, George Soros betting against the Pound or Dalio saying buy gold because the Fed will “monetize” debt.

B) Those who use macroeconomics to build a first principles understanding of how to build a pragmatic asset allocation. Think, Gene Fama saying to buy index funds because beating the market is hard or me telling you to match certain assets to liabilities because we can quantify the asset-liability mismatch of a financial plan.

The people in category A will tend to time the market and use macroeconomics as a tool to try to outsmart the market. They think they can predict when World Wars will occur or when the Dollar will collapse.

The people in category B build a framework for understanding the world for what it is and then diversify knowing that predicting geopolitics is very difficult and that capitalizing on those changes is even more difficult.

These are very different approaches and I consider myself a Category B investor. I understand the qualities that make stocks, bonds and gold function certain ways across time. And then I build portfolios that are diversified because macroeconomics taught me that beating the market is damn hard, costs matter and diversification is the only free lunch. I talk a lot about geopolitics here, but that’s mainly because I am debunking bad narratives about it. For me, discussing Category A is a necessary evil that helps my Category B approach stay the course.

Back to Dalio’s piece though. His big conclusions are – buy gold and sell bonds because the world order is collapsing and that means governments will print money and all that. Again, I don’t know how this is useful. What kind of bonds are we talking about? All of them? Should we not even hold T-Bills? And why are we loading up on gold after one of the biggest runs in history? This was great advice 5 years ago, but what about now? And how do we know the world order will lead to more money printing than what we’ve already seen? Government money printing hasn’t been the main driver of inflation for most of the last 40 years. Demographics and tech trends have driven a persistent disinflationary trend. Is that changing? Are we fully understanding inflation trends solely by focusing on geopolitics? I don’t think so. So the narrative is compelling and emotionally gripping, but it’s not a complete view of important macro trends like inflation.

Speaking of the past – let’s look back at one of the more famous portfolios presented in a similar context – Dalio’s All Weather portfolio from the Tony Robbins book 12 years ago. Remember that one? It was:

30% Stocks

40% Long-term Bonds

15% Intermediate Bonds

7.5% Gold

7.5% Commodities.

Back in 2014 I warned investors about this allocation saying “if I had a gun to my head I’d bet the ranch that this bond heavy portfolio with a commodity tilt generates sub-optimal returns going forward. We know that because the math on the low bond yields and the negative real returns of commodities makes it a high probability bet.“

And yes, this portfolio has been a huge underperformer with 2% annualized real returns compared to 4.5% for global 60/40 and 7.5% for global stocks. The huge long bond allocation just killed the performance. So, I find it all a bit odd that we’re now reversing course on bonds when bonds are vastly more attractive than they were in 2014. I’ll even flip the bet now. I wouldn’t be shocked if bonds beat gold over the next 10 years!

Anyhow, I don’t mean to beat up on Ray. He’s a lot richer and smarter than I am, but I don’t see how these kinds of vague geopolitical narratives are all that helpful without giving readers a much more precise set of conclusions. All the geopolitical stuff is fun to theorize about, but if you think you can predict the madness of foreign dictators then good luck to you. I sure can’t and for me personally, these kinds of articles don’t result in anything actionable. I wouldn’t change one thing about my asset allocation based on an article like this and I don’t think you should either.

2) The Tariffs are Dead! Long live the tariffs!

The big news of the week was the Supreme Court ruling Trump’s tariffs unconstitutional. The market seemed to like the news, but the market has also shrugged off the whole tariff scare since last April. As I’ve explained before, that’s because the tariffs have been mostly a nothing burger in the grand scheme of things. Back in April 2025 when they were talking about tariffs replacing the income tax we were talking real damage because that would have been a $2.5 trillion tax hike on corporations. But our tariff tracker shows that the total amount of tariffs since April has been about $300B. That’s a roughly $220B increase over the tariffs that were already in place. And while $220B of new taxes is not nothing, it’s just 4% of federal tax revenue. So we’re not talking about some budget altering revenue source here.

As it pertains to the specific news here – I also think this is mostly a nothing burger. Trump has all sorts of other avenues through which he can impose fees and tariffs on foreign imports. But instead of being able to utilize the broad emergency tariffs he’ll have to use a patchwork process taking advantage of Sections 122, 301, 232 and 338. These are more limiting and will require more legal battles, but they’re all ways in which he can retain tariffs by working around the IEEPA framework.

In short, this is just more of the same. The tariffs were dialed back bigly when we made the China deal last year and while they’ve been moderately large they have not been a meaningful driver of the macroeconomy.

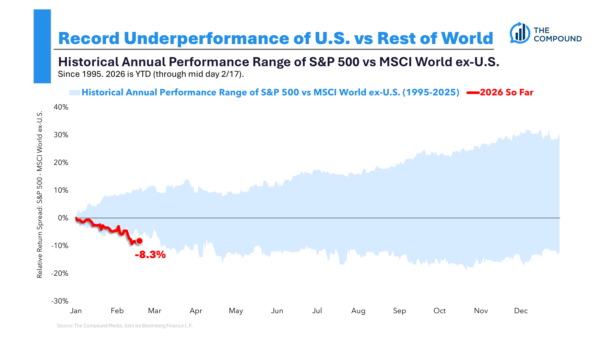

3) The Ex-USA Trade is Winning.

Speaking of the dollar collapse and foreign trade – foreign stocks continue to rip after last year’s huge performance. Foreign developed stocks are up 8.5% year to date while US is up just 0.85%. Foreign stocks have now outperformed US for 2.5 years. And as Ben Carlson notes in this excellent piece, the outperformance in many sectors goes back even longer than that. So, is the US period of outperformance finally coming to an end? Will it continue? I don’t know, but I’d be shocked if we don’t see a broader mean reversion in relative valuations over the next 10 years and that gap is still gigantic.

But the more important factor here is the Dollar. I always talk about how foreign diversification isn’t really a bet on foreign corporations so much as it’s a hedge against the Dollar. When the Dollar declines foreign equities have a strong tailwind and vice versa. So foreign diversification isn’t just a way to diversify away from domestic economic risk. It’s very specifically a hedge against domestic currency risk as well.

If you are worried about the Dollar then owning gold or avoiding bonds is just one way to hedge yourself. You should also be reducing exposure to domestic equities. Of course, as a Category B investor I like to own both foreign and domestic equities because I don’t really know if the Dollar is going to decline against foreign currencies. And I don’t need to make precise macro predictions to benefit from these changes.

4) Bonus Thing I am Thinking About – private markets.

The other huge news story this week was the closure of a private credit fund. I really liked Brian Moriarty’s piece on this at Morningstar, in part because he touches on the inherent asset-liability mismatch that occurs inside funds like these. This is the essential risk to understand in instruments like private equity or credit funds. Because their assets aren’t marked daily you can’t really replicate the performance cleanly in any form of publicly listed instrument. ETFs are magical instruments when you are using instruments inside them that are liquid on a daily basis. But if you try to jam illiquid instruments into these things then the wrapper begins to breakdown. So you can get these huge liquidity mismatches across time.

I don’t think there’s anything wrong with owning a slice of private equity or credit. But you really need to put these instruments in specific temporal buckets when you own them. Their illiquidity could make them superior instruments precisely because of the lock-up in capital. That is, a venture capital instrument is an inherently long duration instrument, but if you allocate capital there you need to know that you’re investing in entities that are start-ups or involved in long-term projects. The lock up is what allows the firms to manage their cash flows and take the risks necessary to generate returns for investors. The same thing is true of most private instruments. If you need money in the next few years and you’re allocating the funds to private instruments then you’re taking a big liquidity risk because the funds have an inherent temporal mismatch.

Anyhow, that’s all I’ve got for you this week. I hope you have a wonderful weekend.