I’ve got a short opinion piece for you this week. I hope you enjoy it.

I see a common narrative in some circles where people argue that the boom in gold and Bitcoin prove Warren Buffett wrong about his investing style. Buffett has long criticized owning gold and Bitcoin so as their prices surge you might be inclined to say his world view has been fundamentally flawed, or at least incomplete. I don’t think this is accurate and I’ll explain why.

Here is Buffett’s view on asset allocation in a nutshell:

“When we took over Berkshire, Berkshire was selling at $15 a share and gold was selling at $20 an ounce. And gold is now $1,600 and Berkshire is $120,000.

But you can take a broader example than that. If you buy an ounce of gold today and you hold it a hundred years, you can go to it every day and you can coo to it, and you can caress it, and you can fondle it—and a hundred years from now you’ll have one ounce of gold and it won’t have done anything for you in between.

If you buy 100 acres of farmland, it will produce for you every year. You can use that money to buy more farmland, you can do all kinds of things, but for a hundred years it’ll produce things for you and you still have the 100 acres of farmland at the end of the hundred years.

You could buy the Dow Jones Industrial Average for 66 at the start of 1900. Gold was then $20. At the end, it was 11,400, but you’d all gotten dividends for 100 years. So a productive asset of any kind—a decent productive asset—is going to kill a non-productive asset over time.

Now, in any given one-year period, five-year period, any asset can outperform another asset—you know, tulips. But I will guarantee you that farmland over 100 years is going to beat gold, and so are equities.”

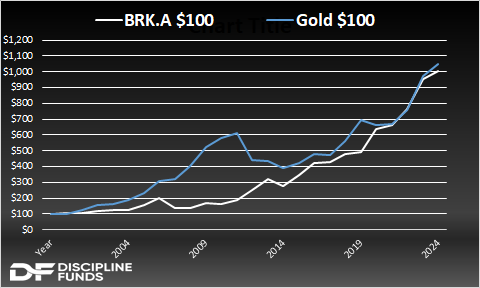

This interview is a few years old, but Berkshire is now worth $748,000 and gold is worth $5,000. Berkshire smashes gold in the long-run, just as he said it would. But one thing I’ve noted at times in recent decades is that Berkshire of today is nothing like the Berkshire of 1965. Berkshire has, for the most part, tracked the S&P 500 for the last 25 years and it has lagged gold for much of that period. So, Buffett has been right in the long-run and wrong in the short-run, right? I still don’t think that’s the right takeaway here.

The bigger problem with unproductive assets like gold is that they have gigantic sequence risk. In my Defined Duration model gold is a super long duration instrument that operates more like insurance than anything else. While gold can operate like a form of portfolio insurance at times, it cannot be relied upon to generate a consistent return that funds your expenses. That’s because you can go thru these humongous real drawdowns and then you get bursts of huge outperformance in certain regimes like the 70s, early 2000s and the 2020-2026 period. But what you don’t get is the consistency and reliability that comes with productive cash flow generating assets. In other words, with stocks you get a consistent stream of cash flow over time that results in more reliable returns so you can more reliably plan your ability to consume in the future. Investors price these instruments more efficiently because there isn’t as much guesswork that goes into whether the instrument has value at certain times.

If we look at the raw data this becomes more apparent. Since 1971 when the gold standard was eliminated, US stocks have generated 7% real returns with 16.8% vol while gold has done 5.2% per year with 19.65% vol. But this doesn’t capture the sequence risk. Gold had a 45 year real drawdown from 1980 to 2025. The US stock market’s longest real drawdown was 12.8 years during this period. The Ulcer Index, which captures this sequence risk better, was 19.25 for the US stock market and a whopping 60 for gold (0-5 is considered low risk, 5-10 moderate, 10-50 high risk and 50+ is considered very high risk). In other words, even if gold beats stocks at times, it exposes the investor to a level of sequence risk that is stomach churning. And it’s precisely because of what Buffett highlights – productive assets generate cash flow from the way the instrument is creating its own internal value so their values are more stable because they yield a more consistent output. When you buy a farm and produce corn the corn itself has its own value that it produces throughout the year. The asset doesn’t fluctuate purely based on the value of the land, but also because of the productive output it consistently creates. Unproductive assets don’t have this embedded stability because they don’t generate a consistently productive yield.

Bitcoin is even more extreme from a sequence risk perspective. The drawdowns aren’t just long. They are gut wrenching with regular 80% downturns. I applaud the Bitcoin Maximalists because they’ve endured a Great Depression style bear market once every 5 years or so. But this is not an asset you would build a financial plan around because the sequence risk is simply too high. So the same basic conclusions apply here. While Buffett probably wishes he’d owned some Bitcoin over the last 10 years the asset itself wasn’t something that Buffett could make reasonable predictions about because there was no underlying cash flow driver from a productive yield.

None of this means that gold and Bitcoin or other alternatives don’t have a potential place in your portfolio. For example, life insurance is a negative cash flow generating asset that has no productive value during the contract’s lifetime, but it could be the absolute most important piece of your financial plan. I think instruments like gold and Bitcoin should be viewed similarly. While you can’t build a reliable financial plan around them you can, where appropriate, still think of them as satellite instruments around a core cash flow plan. Whether these insurance-like instruments are appropriate or necessary for you is a whole other matter.

The broader point here is that the high flying performance of some assets does not prove Buffett wrong. Smart asset allocation is all about probabilistic outcomes that give you certainty of consumption over time. If you need cash tomorrow you don’t put it in stocks, Bitcoin or gold because you know the value might not be there when you need it. But if you need cash in 10 years and you wanted a more reliable sequence of returns then stocks are going to beat gold and Bitcoin in the vast majority of outcomes because stocks have an underlying productive cash flow stream that makes their valuations more reliable when compared to instruments like gold and Bitcoin.