Let’s be honest: no one knows exactly what 2026 will bring. Equity markets could surge or stumble, inflation could reaccelerate or collapse under a shocking recessionary deflation, and unforeseen shocks could upend even the most confident predictions. While the near term is fundamentally unknowable, financial planning still requires us to engage with the future using disciplined, probabilistic thinking grounded in reasonable estimates for key inputs like inflation and long-term stock and bond returns. The goal of this guide is to help you establish those assumptions thoughtfully, so you can plan with clarity and confidence for the years ahead.

Interest rates & inflation

Let’s start with arguably the most important variable in any financial plan – inflation. Inflation has been turbulent in recent years in large part due to the Covid shock. And in many ways we’re still recovering from the shock as the enormous stimulus and supply constraints from Covid filter through the system. Current consumer based 10 year inflation expectations are 4.5%, well above the Cleveland Fed’s expectation of 2.34% and the 10 year break-even rate of 2.3%. This disparity shows the extreme scarring that inflation causes for consumers.

Let’s step back a bit and look at the big picture first.

From a secular perspective, we believe the inflation story is one of extreme macroeconomic headwinds. Global population growth is slowing at the same time the average population is increasing in age. This is a recipe for slowing aggregate demand, a trend that has been in place for the last few decades. Perhaps more importantly, technology is advancing at an unprecedented rate. This increases globalization and puts downward pressure on prices through enhanced supply dynamics. These two trends alone create a secular headwind that makes it very difficult for inflation to surge in the developed world. However, there is a paradox here, in that policy makers will feel pressured to provide increasing stimulus to a global economy that is both aging, more tech-driven, and experiencing rising levels of inequality. I have little doubt that AI will compound these trends in the long-run.

From a market-based perspective, financial planners should rely more heavily on the break-even rate than on the sentiment of consumers. However, the secular risk of significant stimulus means planners also need to assume there will be shocks at times, not dissimilar to the Covid shock. The prior 10 years are a great example of extrapolating this secular inflation headwind and shock environment. Since 2016, inflation has averaged 3.1% per year, as measured by the CPI. Even though inflation was low for most of the period, the COVID shock added significantly to average annual inflation in a disproportionate manner. I think it’s reasonable to extrapolate this sort of assumption into the future for planning purposes, as it assumes a secular inflation headwind, but plans for the risk of shocks along the way. As a result, I would feel very comfortable using a 10-year inflation expectation anywhere in the 3–3.5% range.

Interest Rates & Bonds

The Fed Funds Rate is the key global interest rate benchmark. In 2026 it’s safe to assume near-term rates will decline as President Trump is likely to install a Fed Chief that is amenable to his desire for lower interest rates. While the Fed Chair doesn’t control the overnight rate the FOMC will become increasingly moved to this position. Current Fed Funds Futures are calling for rates close to 3% by the end of 2026 compared to a current effective rate of 3.88%. The longer end of the curve is far more uncertain.

Inflation indexed 10 year bonds are at 1.95%. This is a historically high positive real return over a 10 year basis and implies that we’re not returning to the zero interest rate world of pre-Covid. This means that long-term interest rates are expected to remain stickier than what investors were accustomed to coming out of the financial crisis. This is a more normalized yield curve environment and provides opportunities across the curve that we have not seen in a long time. While many investors assumed bonds were dead after their dreadful performance during Covid the reality is that current real yields offer attractive opportunities for investors relying on safe income. Intermediate US government bonds were up 7.7% with 3.9% volatility during 2025. Not bad for an asset class that has supposedly died. We believe the bond market is not only not dead, but about as attractive as it’s been in a very long time.

At Discipline Funds we rely heavily on T-bills and shorter-term bonds for liability matching needs. In fact, we typically do not like to utilize bonds over 7 years for asset-liability matching needs as we believe long duration bonds are poor liability matching instruments for several reasons.

The primary reason is sheer predictability in a positive real-rate environment – an investor can build a predictable ladder of liability-matched assets using 0–7-year bond ladders, knowing that multi-asset instruments with longer maturities will have a high probability of generating positive real returns over longer time horizons. For example, the investor with a 20-year time horizon does not need a 20-year TIPS matched to liabilities and could harm their own financial planning by going out that far, because the probability of an equity portfolio outperforming a 20-year TIPS over this time horizon is extremely high.

Perhaps more importantly, the investor buying long duration bonds is rarely compensated fairly for such long duration risk. Even in today’s more attractive bond environment the investor buying a 5 year t-note is earning 3.71% while the investor buying a 10 year note is earning just 4.17%. This means the investor buying a 10 year note is taking roughly 2X the interest rate risk of the 5 year note buyer and earning just 0.46% more. This doesn’t make sense to us and the mechanics behind this are becoming quite clear.

The reason for this is fundamentally a function of how our monetary system is structured around the global reserve currency issuer. Long duration government bonds are not designed to fairly compensate investors as they exist in a monopolistic market controlled by the government issuer. While we often hear about “bond vigilantes” the truth is markets have little control over the actual interest rate at which US government bonds are issued as the market can be controlled entirely by the issuer and its central bank as a buyer. The lack of competitive forces in long duration bonds is one reason why, over the last 30 years, modified durations have increased as interest rates have declined – the monopolist is imposing a higher risk instrument on the buyers and indirectly setting its price at the same time. Your reward for risk has deteriorated in long duration bonds because the issuer has no need to compensate you for the temporal risk you are taking. Therefore, what investors traditionally refer to as the “term premium” is not nearly comparable to something like the equity risk premium because equities exist in a fundamentally competitive market where the members of an index like the S&P 500 get removed by superior entities, whereas total bond markets like the US total bond market are becoming increasingly dominated by the largest monopolistic issuer and that issuer is force-feeding longer duration bonds on the market, because it can, and total bond market funds have to reflect this issuance regardless of the lack of competitive forces.

The conclusion from this is that long-term rates are, from a secular and operational perspective, unlikely to move materially higher without significantly higher inflation that forces the Central Bank to maintain a much more restrictive interest rate policy stance. Instead, short rates are likely to move lower while long rates fail to properly compensate investors for the risk they are taking, thereby resulting in a steeper curve, but a curve that is not providing long duration investors with a sensible matching option. This could change if inflation dynamics change materially or short rates re-enter the ZIRP environment, but for now investors are far better compensated for risk in the shorter end of the curve. This has important financial planning consequences as the use of long duration bonds is likely to expose investors to unnecessarily imbalanced risk relative to return.

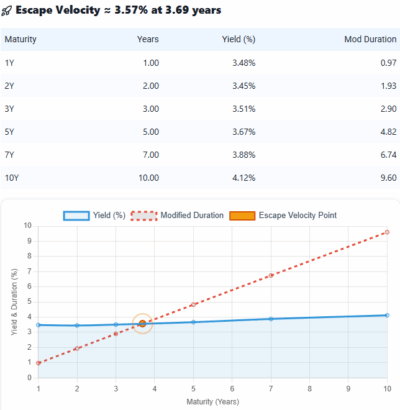

From a risk/reward perspective we like to use the concept of bond market “escape velocity” to judge the risks across the curve. The escape velocity is the point on the curve where your duration, or interest rate risk, is offset by your current yield. This point is presently at 3.75 years. At this point on the curve a 1% shock in rates would be fully offset by the interest earned over a one year period. Instruments with much longer maturities offer increasingly worse risk adjusted returns relative to their potential sequence of returns risk and should therefore be matched to liabilities with caution. You can use our escape velocity tool to monitor this in real-time.

Global Stock Markets

We have no idea what stock markets will do in 2026! Stocks are fundamentally long duration instruments and forecasting their various gyrations in the short-term is a guessing game. On the other hand, we can make fairly reliable estimates about long-term returns. The most common forecasting method is using an extrapolative expectations method by extending past returns into the future. In the last 50 years global stocks have generated 5.8% real returns, US stocks have generated 6.8% and foreign stocks have generated 4.6% per year. It’s not a coincidence that the majority of analysts will forecast an S&P 500 target of roughly 7500 for year-end 2026. That is merely the nominal annual average. This isn’t a bad approach, on average, however it is a bad approach in any single year as the dispersion of annual rates is rarely close to the average long-term rate.

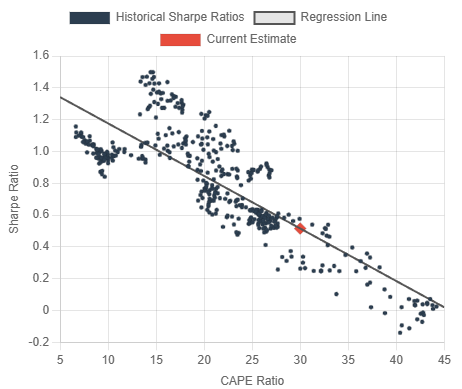

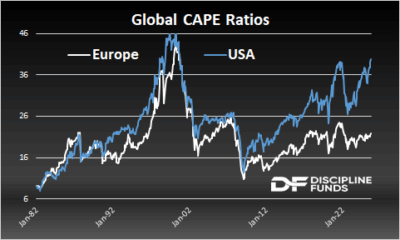

The historical disparity in returns across domestic and international stocks has coincided with an extraordinary divergence in valuations as well. And while valuations are an imperfect forecaster of future nominal returns they do tend to correlate strongly with future risk adjusted returns. The following chart shows the correlation between current valuations and future 10 year risk adjusted returns. In our Defined Duration methodology this is quantified as sequence of returns risk, or the potential inflation adjusted temporal drawdown risk currently embedded in an instrument. Higher valuations will tend to involve high sequence risk that requires care when matching assets and liabilities. For instance, you wouldn’t want to match the Nasdaq 100 to a 10 year liability given that technology currently has a far higher Defined Duration than something like international value stocks. This doesn’t mean you shouldn’t own technology stocks, however. It simply means you shouldn’t match technology stocks to short-term liabilities. And in fact, if you have a very long time horizon we would encourage investors to be very optimistic about technology as we are big believers in the AI boom and the widespread economic transformations it will bring in the decades ahead. But the road to transformation will not be a smooth one.

Current global valuations are high by historical standards. Therefore, stocks as a whole expose investors to higher levels of sequence risk than average. This doesn’t mean you should abandon your stock allocation by any means, but it does communicate that investors might need to be more patient with the way their stock portfolios generate returns, as high valuations are consistent with high expectations which means that even minor economic or market shocks cause higher than normal volatility (even if nominal returns are not lower than average). Therefore, equity investors who are more time sensitive should allocate to equities with a lower probable sequence risk while truly long-term investors could benefit from being aggressive and losing their brokerage firm passwords for a decade.

Our current stock market Defined Durations, based on global equity markets, are as follows:

US Stocks: 28 years – sequence risk is very high.

Global developed stocks: 18.5 years – sequence risk is above average.

Foreign developed stocks: 11.5 years – sequence risk is below average.

This is even more pronounced within markets like the US market where tech stocks have a Defined Duration of 30+ and US value stocks have a Defined Duration of just 14. The aggressive investor with a very long time horizon can own growth and technology with more confidence as they have the ability to ignore any near-term volatility that might coincide with high valuations. The more time sensitive investor should approach those sectors more cautiously. Inequality isn’t just a wealth and income phenomenon – it has very much become a stock market phenomenon and it’s reasonable to assume that style investing is more important than ever for the investor who is trying to construct a time sensitive equity allocation.

The broad conclusion from this is that there is currently a historic disparity in where you are getting your potential sequence of returns risk in the stock market and so diversification is more important than ever for the purpose of temporal diversification and those who are implementing asset-liability matching methodologies.

Alternatives & Portfolio Insurance

Financial planners are often skeptical of alternatives because they can be difficult to allocate inside of a formal financial plan aside from a more speculative role. We don’t utilize alternatives for our base cases because they serve as optional satellite instruments in our asset-liability matching process, that resemble insurance more than anything else. This would include instruments like gold, Bitcoin, managed futures, options, etc. This doesn’t mean there are no use cases for these instruments, however, you just need to be mindful in utilizing them based on a case by case basis.

For financial planning purposes there are specific cases where the use of such instruments can make sense. For instance, a renter who has little to no real asset exposure might consider a commodity allocation in their portfolio. An investor with acute dollar or fiat currency exposure might consider a Bitcoin allocation. An investor who is behaviorally biased towards guaranteed outcomes might consider a low cost options writing strategy. And managed futures can serve as good non-correlated asset class hedges for investors who know they need to own the stock market, but want some potential uncorrelated hedging.

You’ll note that the in the scope of commodities we specifically refer to “commodities”. The inequality of returns hasn’t been a stock only phenomenon. In 2025 gold was up 63% and silver was up a whopping 156%. Meanwhile, the Bloomberg Commodity Index was up 18%. For investors using commodities as portfolio insurance diversification is as important as ever as these types of eye watering returns create significant short-term risks.

On the other hand, we would also argue that when real rates are positive the best form of insurance an investor can own is Treasury Bills as they give you certainty of time, principal and a real return. That’s damn hard to beat even if the risk/return has deteriorated in recent years. In short, alternatives can be useful in specific financial plans, but should be utilized strategically on a case by case basis.

Liability Management

We spend a lot of time in this business talking about asset management, but we too often ignore liability management. This is a curious omission in the process of financial planning considering we can’t always control the returns we get from our assets, but we can more precisely control our liabilities. Liability maintenance has become increasingly important in recent years as inflation has surged. So let’s discuss some of the most important liabilities we all encounter and where some financial planning might make a difference.

Mortgage rates and buying versus renting

Inequality is nowhere more apparent than it is in the real estate market. Investors who purchased a home before the Covid real estate boom have benefited from a once-in-a-lifetime boon as mortgage rates surged and prices surged. For the investor who mortgaged their home at low interest rates this not only served as an incredible inflation liability hedge, but it has been a huge benefit to net wealth via asset appreciation.

When viewed through the lens of a Defined Duration perspective the appreciation is unlikely to last. Homes are long duration instruments that rarely appreciate at high levels. In the last 40 years residential real estate has generated 1.5% CAGR in real terms. Since January of 2000 the real CAGR has been 4% per year as housing surged over 50% in nominal terms. In other words, Covid pulled many years and perhaps even decades of appreciation into the present. As a result, residential real estate has been a laggard in recent years and has generated negative real returns since June of 2022.

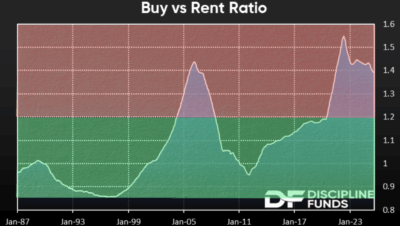

The kicker here is that rental rates remain relatively subdued by comparison. And with rental prices at much more affordable levels and wages growing only modestly, the low appreciation of real estate is highly probable for the foreseeable future. Our general view is that rental rates will rise while home prices stagnate which, at some point, will create some equilibrium. If this coincides with lower mortgage rates in the future, buying will become much more attractive. But for now, we see no reason for homebuyers to be impatient for financial reasons. The attached chart shows the extreme disparity in the buy:rent ratio. Current levels are extremely high and while this should be properly viewed as a sliding scale of relative affordability I am presenting it in red light green light format because my daughters are currently playing red light green light behind me.

I always like to communicate that owning a house is a personal decision for the needs of your family and comfort. And nothing is more important to the financial plan than the happiness of the family. Housing should never be a pure financial decision. But for now the financial argument for buying a home remains a relatively weak one as appreciation is unlikely to outperform a diversified portfolio of stocks and bonds in the years ahead.

At the same time, for the homeowner with a higher cost mortgage we should see an improved refinancing market in the coming years. A Fed with a bias towards lower rates will want to get benchmark rates lower to help consumer borrowing and borrowers who can pounce on lower rates should be ready to take advantage in 2026 and 2027.

Electricity

Electricity prices have been one of the stickier elements of inflation in recent years. The latest rate of change was 6.9%, well above headline inflation of 2.7%. This is likely to become an increasingly controversial dataset as AI datacenters suck up more and more power in the years ahead. The AI boom is here to stay and so our baseline estimate is that electricity costs are one component of CPI that is most likely to remain sticky.

Consumers would be wise to consider alternative energy sources as solar and battery powered units become increasingly efficient. This is likely to become much more magnified in the years ahead even as alternative energy sources continue to come online.

Healthcare, food and entertainment

We’re not healthcare gurus and this isn’t a self improvement report (well, not directly), but it’s safe to assume that the cost of healthcare isn’t going down any time soon. While this is intended to be a long-term financial planning report, the truth is that the very best hedge you have against healthcare costs is to be meticulous about your short-term diet and exercise. Since we’re not healthcare gurus I’ll just point you in the direction of someone who is.

As for food, again, we are not food experts. In fact, in college I once froze and then microwaved sushi for my now wife, when she told me it was her favorite food. While I am an old fashioned steak and potatoes Irishman, I have to admit that 2026 will be a year where “eat food, not too much, mostly plants” will be a goal of mine. Given the surging price of beef I suspect many of you will follow a similar plan, perhaps not by choice.

Entertainment – “cut the cord” is about to turn into “ream the streams”. Last week’s NFL games required 7 different streaming services to get access to all the games. It’s absurd. No one needs this and no one wants it. The cost of other entertainment has skyrocketed as well. I think it’s time for more of us to go outside and touch some grass with one another and be more mindful of experiences that are more interpersonal and less based on technology being injected into our brains. I recently canceled my YouTube TV out of spite. 2 months later I can tell you that it has had absolutely zero negative impact on my life. /oldmanrantover

Taxes

Smart tax planning has become more important than ever in a world of rising and more complex taxes. This is especially important for investors with complex estates and capital gains. Some tax considerations to help control your 2026 liabilities include 351 exchanges, Roth conversions, qualified charitable distributions via RMDs, tax loss harvesting and others.

The 5 Pillars of Defined Duration

Let’s pivot to asset-liability management more specifically .

Good financial planning is all about giving people certainty of consumption across time. We like to view our financial lives across five specific time horizons that can be matched to certain assets in a more granular, planning-based asset allocation. Each time horizon can be granularly customized to provide a more precise and retail friendly version of asset-liability matched portfolio management, not dissimilar to the way many institutions implement asset-liability matching processes.

These time horizons are 0-3 years, 3-7 years, 7-15 years, 15+ years and perpetual (if needed).

0-3 years: predictable near-term consumption and emergency funds

Key Theme: Real returns are likely to compress in short duration instruments as the Fed will reduce interest rates further. This will make the shorter end of the curve less attractive on a relative basis.

Considerations: Investors should consider tilting further to the longer end of the 3 year range. “T-bill and chill” remains an attractive strategy, but 2-3 year notes, TIPS and shorter maturity constant maturity ETFs are solid options. Alpha Architect’s BOXX ETF is an innovative option for investors who can wait 12+ months to let long-term capital gains accrue. We would overweight the long end of the 0-3 year spectrum as much as possible.

3-7 years: near-term expenses, typically lump sum consumption needs like new cars, house down payment savings, retirement bridging, etc.

Key Theme: As mentioned above, 3.75 years is the escape velocity point in the bond market so this is currently a very attractive point on the curve. Real yields are especially attractive in this range as 5 years TIPS yields are 1.5%. With the short end likely to compress the belly of the curve is especially attractive from a risk/reward perspective.

Considerations: Investors with short-term needs and more temporal flexibility should consider larger allocations here compared to the 0-3 year range to lock in ladders and slightly longer maturities. Government bond ladders in the 3-7 year range are solid options. TIPS are especially attractive in this range as is any instrument with a defined duration or constant maturity of about 5 years.

7-15 years: moderately long-term expenses such as near-term retirement, college planning, etc.

Key Theme: Instruments in this time horizon, including instruments like a 60/40 portfolio, are exposed to higher than normal equity risks as the stock market’s defined duration rises with valuations. This creates higher than normal sequence risk in this segment which requires more thoughtful duration control. The 7-15 year time horizon is also where the Global Financial Asset Portfolio exists and is, in our view, the most difficult time horizon to plan for because it isn’t long enough to just own equities and isn’t short enough to only own T-Bills or bonds. And with soaring equity valuations it even makes default allocations like 60/40 somewhat difficult to digest.

Considerations: Vanguard recently noted that investors should consider tilting 60/40 to 40/60 due to higher than normal equity market risks. This is, interestingly, what John Bogle also advocated on occasion. This is a reasonable consideration if it can be done in a tax efficient manner, but also needs to be done in the proper temporal context. In the current environment a 60/40 of global stocks and bonds comes in as a 16 year instrument in the Defined Duration approach while a 40/60 comes in at a 12 year instrument. In other words, it’s reasonable to assume that a 60/40 will expose you to higher sequence risk. This is only relevant to the investor who is sensitive to sequence risk and many investors might be indifferent to this across a 7-15 year time horizon. But given the disparity in global equity valuations we would consider a global allocation at a minimum, whether that be 60/40 or 40/60.

15+ years: long-term planning such as long-term retirement goals, multi-generational needs, etc.

Key Theme: Long time horizons offer the most flexibility for risk taking. As we noted above we are big believers in the transformative nature of AI. But investors owning AI related instruments must be increasingly time sensitive as the ultra high valuations create more potential sequence risk.

Considerations: For the equity investor who wants more certainty and lower sequence risk domestic value, domestic low volatility and international equities are especially attractive. With domestic market cap weighted instruments becoming increasingly concentrated in AI names investors should beware of potentially higher sequence risk here as well. One interesting aspect here is that foreign equities generated nearly 2X the return of US equities in 2025 without valuations compressing. We wouldn’t be surprised if this becomes more common in the coming decade until valuations mean revert meaningfully.

Perpetual: insurance for the unknown time horizons.

Key Theme: With outsized geopolitical risks and unusual valuation disparities, the case for portfolio insurance has become increasingly reasonable. AI creates unusual economic opportunities and risks. The world is changing faster than I can ever remember and companies will grow and collapse faster than ever. It’s an exciting and scary time to be alive.

Considerations: Life insurance is of course the key consideration here. “Buy term and invest the difference” is the old motto and it’s as true today as it was when my career started. As for portfolio insurance more specifically, we would heed to comments above. This is a very personalized decision that is dependent on personal circumstances. The decision to venture outside of traditional cash flow generating instruments should be done in accordance with financial planning and behavioral needs, not speculative guesses about what may or may not happen in the future.

Key Risks and Trends we Don’t Love

New Issue Risk #1: The rise of the distributed income fund

There has been a boom in “distribution yield” funds. This is typically done in option writing strategies where current income is being earned from the portfolio in exchange for some sort of more certain future outcome. In the vast majority of cases the guaranteed outcome is that you’re capping, or giving up some total return upside, in exchange for current “income”. In addition to being typically less tax efficient these instruments are also higher cost and much higher cost when you quantify the opportunity cost compared to owning the underlying index and simply harvesting gains as long-term cap gains on occasion for your own “homegrown dividend”. We would be very selective about the surging popularity of these instruments as they are not true income generating instruments in the traditional sense.

New Issue Risk #2: Leveraged ETFs.

Leverage can be a very good thing when used intelligently. We mentioned above that the best inflation hedge of the last 5 years was a heavily mortgaged home. But in recent years we’ve seen a boom in single stock leveraged ETFs. These instruments are purely speculative. They have no business in any sort of financial planning based approach as they compound the difficulty of stock picking with higher taxes and fees than this process already involves. The surge in the “degenerate” gambling approach to markets is concerning. Financial markets should be approached as long-term positive sum games and not short-term negative sum games.

New Issue Risk #3: Private credit funds.

The lagging performance of bonds in recent years has resulted in the rising popularity of private credit instruments. We believe this is a spot to be very selective. When done in an ETF wrapper this is a very difficult and inefficient instrument to own because the underlying assets simply cannot be marked-to-market consistently. This makes the ETF wrapper look more and more like a closed end fund labeled as an ETF. With public bond funds again yielding relatively attractive yields this is a segment we would approach with caution.

Legitimate market risks #1: Valuations.

We’ve discussed this enough already. But it’s important to emphasize what high valuations really mean. They do not necessarily mean lower future returns. But they could mean more temporal and sequence risk as the risk adjusted returns could be lower in the future. For instance, it’s very possible that the Nasdaq 100 generates 10% per year for the next 10 years. But if that comes with 2X the normal historical volatility then the instrument has exposed you to very unusual sequence and behavioral risk. It’s a legitimate concern and planners should be mindful of this primarily for behavioral purposes. Setting the right temporal expectations is essential to good behavior.

Legitimate market risks #2: Geopolitical risks.

The war in Ukraine and consistent hostile talk about Taiwan creates a very unusual geopolitical environment. At the same time we have a United States that is becoming increasingly isolationist. We don’t spend a lot of time trying to predict the unpredictable mood swings of politicians, but increased geopolitical risks are just another reason to maintain a diversified financial plan. This is one more reason to consider broad diversification. As Morgan Housel says, “risk is what we don’t know” and geopolitical risk is the ultimate unknowable.

Legitimate market risk #3: Artificial intelligence.

The impact of AI is still very much up in the air. We are big believers in its positive impact, however, the degree to which this is positive and negative is going to be extremely uneven. From my perch it appears to be occurring faster than expected, especially in the robotics space. And that’s where things could become very messy. After all, for now AI is merely making current workers more productive. So it’s not resulting in mass layoffs. It has slowed hiring as firms get more from less, but firms aren’t firing heavily because of this. So employment growth as slowed, but not contracted. But when the robots come online you’ll see this trend become much more negative. And that’s a world where the government likely gets much more involved in various ways. Our view is that inequality will worsen, political tensions will increase and many of the trends we’re seeing today will become much more exacerbated.

Narrative risk #1 – The collapse of the Dollar.

Perhaps the most common question I have fielded over the course of the last 20 years is “is the US Dollar going to collapse?” The short answer is no. It won’t collapse because there is no reasonable alternative. And I am sorry to rain on any Bitcoin parade, but we’re 15+ years into the Bitcoin experiment and it has made virtually no dent in the global payments system, at least as far as it concerns relative US Dollar usage. Payment processing is far from Bitcoin’s best use case and doesn’t appear to be a threat to the Dollar at all.

In terms of Dollar reserve status, there is simply no alternative. The RMB is not widely trusted. The Euro doesn’t have the economic might to support its widespread use. And so the USD remains the cleanest shirt in a closet of dirty fiat currencies. I don’t see how this will change any time soon without a collapse in US economic dominance. And that seems to be accelerating, not decelerating in recent years….

Narrative risk #2 – Short-termism.

It would be a narrative failure of my own if I didn’t close out this note with a brief mention of time. It is, after all, the most valuable thing we all have and the reason you’re reading this note in the first place. We’ve discussed many time horizons in this note because we live our lives across many time horizons, of which the short-term is the most important. But as a new year comes around the corner I’d encourage you to set long-term goals that are achieved through disciplined short-term actions. In the world of portfolio management the best short-term actions you can often implement is the act of nothing. Yes, all portfolio management requires some activity and we actually encourage short-term management of short-term instruments. But know your time horizons and remember that the most sustainable wealth creation is done over the long-term through many short-term consistent and disciplined actions. Also be keenly aware of the relationships between your liabilities and your assets across time. It will help you sleep better at night and help you maintain a more planning based and organized process through a financial world that is becoming increasingly complex to navigate.

Conclusion

The world is becoming an increasingly uncertain place with rising geopolitical risks, rapid technology changes, surging inequality and a constantly shifting/hostile public policy debate. Good financial planning is more important than ever. I hope this report provided you with a little bit of clarity in an increasingly uncertain world. And of course, I hope you have a wonderful and very disciplined 2026.