Here are some things I think I am thinking about this week.

1) The Paradox of the Expectations Demand Curve.

I’ve been grappling with the current sentiment around the economy and why so many people feel so disgruntled by it all. Is it a Covid hangover? Are living standards actually getting worse? Or is there more going on here than we might think?

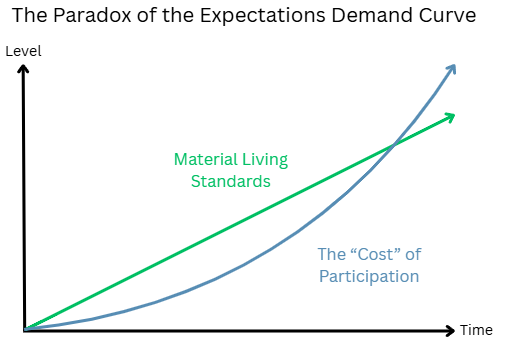

On the one hand, I think it’s undeniable that living standards have gotten better over the last 50 years.1 I write about this all the time and the data to me is virtually irrefutable. But if this is true then why is sentiment in the toilet? I think I’ve distilled this down to a simple idea that I am calling the Paradox of the Expectations Demand Curve. Here it is in visual format:

This chart shows that two things are true: 1) living standards have gotten significantly better overall. And 2) the cost of accessing those living standards has increased as fast and for many it’s increased faster. I write “cost” in quotes because the cost is subjective in many ways. For example, the internet has improved our lives in countless quantifiable ways. But it has also had a cost in mental health for many. We do not quantify mental health in economic statistics though so you might see a quantifiable increase in living standards that comes with a more subjective cost. And then in other cases, like housing, the physical cost of getting access to all the improved housing in the world has gotten monetarily more expensive. So you have both tangible and intangible costs here that have increased.

The key point is that over time, what society offers keeps getting better (green line shoots upward), but the price and expectations (in stress, money, status competition, complexity, and mental health) you must pay to actually enjoy those higher standards rises almost as fast or faster (blue curve). So, absolute living standards increase, but your relative living standards might not feel like they’ve increased because you’ve paid for that increase in varying ways.

I don’t actually know where we are on that curve at this point and different people experience the relationship differently. But it sure feels like the blue line is above the green line for most people. And what worries me is that I don’t know if it’s reverting any time soon because in a world of AI we’ll very likely see the green line continue to go up, but getting access to all the coolest parts of that green line will continue to increase even faster.

2) QE Begins Again! NOT!

The big news of the week was the Fed cutting rates and the restart of what many people are calling “Quantitative Easing”. Now, I don’t want to sound arrogant and say that I was the very first person to say QE doesn’t cause inflation. But I did spend about 10+ years saying this as soon as the policy was unfurled in 2008. And we did end up getting 10 years of low inflation after that. It was one of the great conundrums at the time and there were all sorts of poor explanations (low velocity, banks not lending reserves, interest on reserves, etc) that missed the point.

The main point I made back in 2008 was quite simple. When the Federal Reserve buys assets from the private sector they change the composition of private sector assets, but not necessarily the quantity. For instance, let’s pretend ABC Bank holds $100 of T-Bonds and the Central Bank decides they want to buy $100 of T-Bonds for whatever purpose. They do this by creating new reserves and effectively printing them into the bank’s account. The Central Bank removes the bonds from the economy and holds them on their balance sheet and the bank now has $100 of reserves. The kicker is that those T-Bonds were already printed into existence from some past deficit spending. So, when the Central Bank buys them it’s really no different than the US Treasury going back to you and handing you a T-Bill in exchange for the bond they previously issued you. In our example here, the bank is no better or worse off than it was before because they have the exact same net worth that they had before. You might claim they have more “money” in some technical sense, but they didn’t get richer, get more income or obtain more net financial assets in the process. I used to always say that QE is like swapping a savings account (T-Bonds) for a checking account (reserves). You don’t go out and spend more when you exchange a savings account to a checking account so why in the world would QE cause some quick rush to spend money? It doesn’t! This is the basic reason why QE doesn’t cause inflation. All else equal, it changes the composition of outstanding assets, but doesn’t change the quantity.

And this was really the big lesson coming out of the GFC. What changes the composition of net financial assets is fiscal policy. When the government runs a big deficit they are issuing net new financial that increases the size of the private sector balance sheet. This is the real asset printing, as I like to call it. And we know from Covid, that it can cause high inflation. This was the key difference between the Covid policy response and the GFC response. Both of them involved huge QE programs. But only one of these environments included a massive expansion in government expenditures (government expenditures as a % of GDP went up from 20-25% during the GFC and 20-45% during Covid). This is definitive proof that QE doesn’t cause high inflation unless it occurs with a coinciding surge in government spending. And that makes absolute sense, both from a basic accounting perspective, and now an empirical evidence perspective.

This doesn’t mean QE has no simulative effect though. QE is designed to lubricate the banking system with more reserves and arguably has some side effects like creating more demand for other assets. But in and of itself, QE isn’t the inflationary bazooka-like “money printing” policy that so many people make it out to be.

Anyhow, I don’t care if people call this QE or not. The bottom line is that this was more so about lubricating the plumbing of the banking system than anything else. So I don’t think it will have a big impact on overall inflation.

3) Is It a Bubble?

Here’s the best thing I read this week. It, unsurprisingly, comes from Howard Marks. Marks has a very balanced way of assessing the current environment and it roughly aligns with my view. His primary conclusion is this:

“Since no one can say definitively whether this is a bubble, I’d advise that no one should go all-in without acknowledging that they face the risk of ruin if things go badly. But by the same token, no one should stay all-out and risk missing out on one of the great technological steps forward.”

I would only add one wrinkle to this – time. Bubbles generally aren’t wrong. The Nasdaq bubble wasn’t wrong. It just shifted the fabric of time and space by bringing expectations so far into the present that you got really uneven returns for a long time afterwards. The euphoria over the internet in 1999 was absolutely right. It was just really early. And that’s the risk of investing in a frothy market. It doesn’t mean the market is wrong in the long-run, but it does expose you to the risk of being wrong in the short-run.

That’s why I talk a lot about sequence risk here. Sequence risk, the manner in which you generate your returns across time, is everything to an investor. We all want the most return in the shortest period of time. But stocks generally take a long time to generate high returns. And things like T-Bills generate stable returns over short periods of time. You have a temporal trade-off in risk assets. This is also why I harp on asset-liability matching so much. When your strategy is based around time you don’t have to worry about timing the market. And if you’re strategically diversified across time horizons bubbles become a lot less relevant to you because, if you hold a frothy part of the market in your portfolio, it should be properly aligned with a long-term component of your portfolio.

Anyhow, Marks is typically great so go have a read. And as always, stay disciplined.

1 – Some people might pushback on this, but the facts are the facts: in the USA since 1975 life expectancy has increased from 72 to 79, infant mortality has fallen from 16.1 to 5.4 death per 1,000, real median household income has increased from 62K to 80K, poverty rate declined from 18% to 7.5%, violent crime fell from 473 to 363 per 100K and this is before we even start dipping into things like the amazing technological advancements. I mean, I can order something that I didn’t even know existed at 8AM and it arrives by 12PM. I can get a ride in a self driving car. I can fly across the country in 5 hours while I watch Netflix on a supercomputer in a seat in the sky. This isn’t to say that human life isn’t hard at the same time. But I find it hard to believe that this isn’t the very best time in human history to be a human being.