Here are some things I think I am thinking about during my Turkey Day hangover.

1) $140,000 is the new poverty level!?!?!

Mike Green wrote a viral post earlier this week in which he argued that the new poverty line is as high as $140,000. The article resonated with people and was widely praised. I told Mike that I thought his reasoning was a bit hyperbolic (he did not appreciate this), but the hyperbole is also what made it go viral. At the same time, despite it being hyperbolic I do think Mike is making an important point.

On the one hand, the article is filled with inaccuracies. Michael Strain, Jeremy Horpedahl and Scott Winship all wrote sweeping critiques of the piece that detail the errors. The most basic flaw in the piece is that Green created his own cost of living index (with spurious estimates) and then refers to this as the new “poverty line”. The problem is that the poverty line measures a level of economic destitution, not median cost of living. Green’s figure is actually a metric of what it takes to be financially comfortable in the wealthiest advanced economy in human history. It is so far from being a metric of destitution that it might actually be generous of me to refer to it as being mere hyperbole. But that doesn’t mean Green isn’t making a salient point.

The reason the article resonated with so many is because, despite its errors, there is a lot of truth in the idea that we’ve structured an economic system which has created what Green refers to as a Death Valley. That is, the system has a perverse incentive structure that doesn’t help lift people out of the valley and even rewards them for staying in it. The result is a sort of perpetual inequality that doesn’t rebalance itself and in fact becomes structurally worse as time goes on. As Green says, you’re either rich enough not to care or poor enough to actually benefit. The middle class get caught in the, ahem, middle, and feel like they can’t advance and in fact oftentimes feel like they have no incentive to do so. It’s not great.

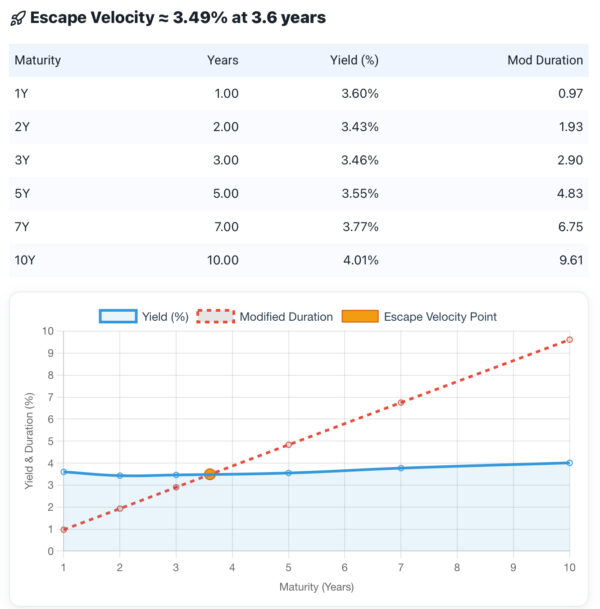

2) Updating Bond Escape Velocity.

It’s been a rollercoaster 5 years for bonds, but 2025 has been a definitively good one so far. The aggregate bond index is up 7.6% YTD with just 4.5% volatility. Now, I’m old enough to remember all the way back to 2023 when bonds were declared dead by many people, but they’re up 4.8% CAGR since the beginning of 2023 and now approaching all-time nominal highs. Not bad. And that’s the nice thing about bonds – no matter what the scary narrative about them might be they’re grounded in math, not narrative. For example, back in 2023 I said that bonds with a duration of less than 5 had reached what I call “escape velocity” – that is, their current yield was higher than their current interest rate risk, which made them a relatively attractive instrument on a risk/reward basis.

Speaking of which – here’s a little teaser of the tool suite I am releasing in the coming weeks. This particular tool will update the escape velocity in real-time. It does this by capturing the real-time modified duration compared to the current yields across the government bond market. This is the theoretical optimal point on the yield curve at the moment because it’s the point where your current yield is equivalent to your current interest rate risk. So, even if rates rise by 1% in the next year you’re earning enough income where you’re still at nominal break-even. The tool will update in real-time to give us a snapshot of what the risk/reward looks like across the curve. At present it’s saying about 3.5 years is the optimal point. In this context, where the blue line is above the orange line you’re experiencing “escape” income.

There’s a lot more where that came from. I’ve built about 20 tools in the last few months that are similar to this. I think you’re going to find them really useful.

Anyhow, bonds aren’t quite as attractive today as they were at 5% yields, but you’re still getting a real return across most instruments inside of 5 years so if you’re using an asset-liability matching strategy then this is still a very attractive place to be for safe income.

3) Avoiding Narratives with Asset-Liability Matching.

Speaking of asset-liability matching. I am going to release the basic version of HourglassFP, our new ALM software, this week. This might be my favorite thing I’ve ever built. It will take an income statement and balance sheet analysis, run a completely quant-based risk profile on you and then spit out an asset allocation that is diversified and time-weighted based on your financial plan. It’s very cool. I don’t think I’ve ever seen anything like it. The risk profiler alone is a huge step up in the way risk profiling is done at present, but the fact that it spits out an ALM portfolio is icing on the cake.

My favorite thing about it is that it’s almost entirely quant-based. It’s data in and data out. No narratives, no opinions, none of that. Which is what I’ve always been looking to construct because the narratives are the hardest part of the investing process.

I’ve written thousands of articles over the years debunking nonsense because these articles give people a more balanced perspective about what the real risks they’re exposed to in the financial markets. For 20 years I’ve felt like I am fighting with a hyperbolic news stream that wants to derail every one of my clients from owning stocks and bonds. I write these debunking pieces because I feel Iike I owe it to our investors to give them pragmatic perspectives about a hyper-emotional topic – money.

And while I’ll still be writing those articles they’ll now operate more as a complement to the quant-based methodology we’ve constructed. That way your financial news consumption becomes something that informs you and gives you perspective and comfort instead of thinking it’s a way to react (and overreact) to every market move you hear in the media.

I hope you all had a wonderful Thanksgiving. I think I might not eat for a week. I wasn’t very, ahem, disciplined, yesterday. I guess now that I am nailing down this quant-based ALM approach I need to figure out some way to make my diet more systematically disciplined. Or maybe not. There are certain things in life where too much discipline can be counterproductive.